المدة الزمنية 15:15

Option delta plus gamma (FRM T4-16)

تم نشره في 2019/02/26

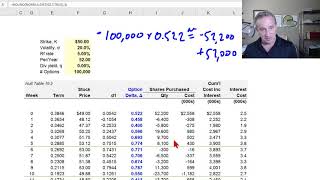

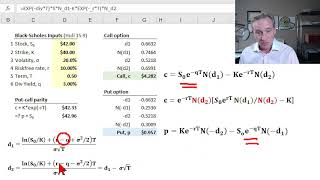

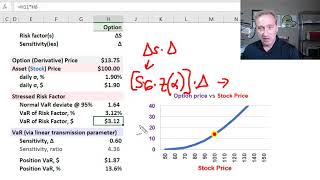

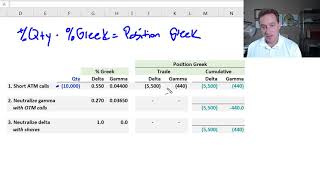

[my xls is here https://trtl.bz/2tIZxr7] Position Greek = (+/-) Quantity * Percentage Greek. If we are short a call option, then we are short position delta and short position gamma. If we are short a put option, then we are long position delta (ie, negative quantity * negative delta = positive) and short position gamma (ie, negative quantity * positive gamma = negative). To be short gamma is to be exposed to large jumps; aka, short volatility. Discuss this video here in our FRM forum: https://trtl.bz/2Es4zOR

الفئة

عرض المزيد

تعليقات - 6

مقاطع الفيديو ذات الصلة على Option delta plus gamma (FRM T4-16):